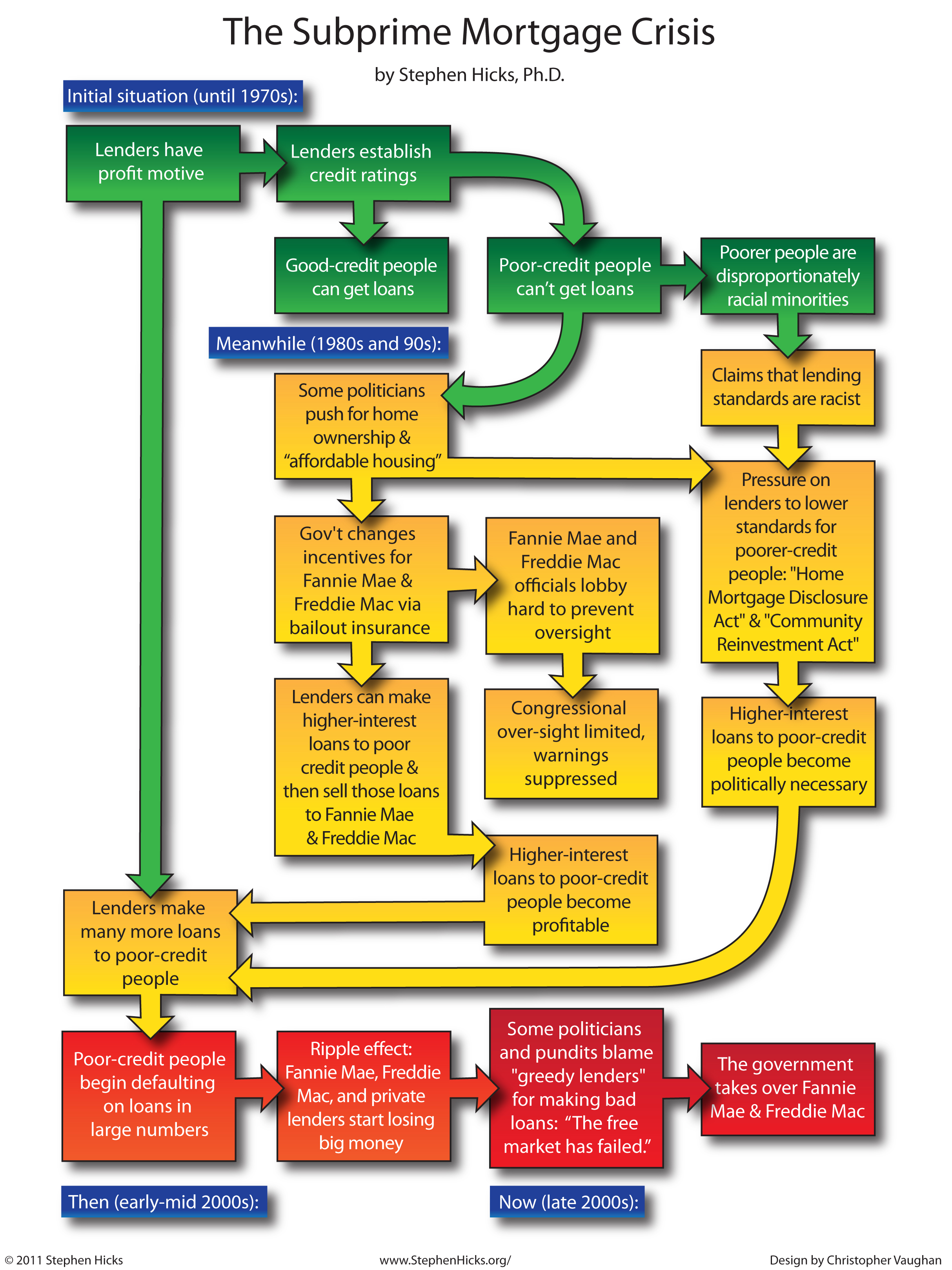

Here is a simplified flowchart, developed for my business ethics courses,  reflecting my understanding of subprime mortgages’ contribution to the crisis.

reflecting my understanding of subprime mortgages’ contribution to the crisis.

Let me emphasize that this is only about the subprime contribution of the overall crisis. Fannie Mae and Freddie Mac enabled much spillover into non-subprime mortgage sectors, government-set capital requirements and other regulations enabled the AAA ratings of mortgage-based securities that encouraged speculators, and there were plenty of imprudent and unscrupulous characters in the private sector too.

Click on the image for a larger size or here for a PDF version.

{kind=link}

Suggestions for improvement welcome. Thanks to Christopher Vaughan for the flowchart’s visual design. [Return to the StephenHicks.org main page.]

The existence of $1.4 Quadrillion in derivatives, corrupt ratings agencies, and the existence of the central banks’ fiat monetary system underpinning a fractional reserve Ponzi scheme did not help either.

There is no doubt that lending more money to poor people than they could afford did not help the economy, but that was probably a relatively minor component in the overall weakness and instability of the financial system.

When you have firms like Goldman Sachs buying up derivatives for their own toxic products, you have demonstrated what amounts to insurance fraud. How would you feel if your realty agent was taking out insurance for the house it just sold you? The private financial firms used derivatives to reclassify risky mortgages into AAA ratings. When the whole thing fell down it was AIG (The insurance agent) holding the bag, and the first firm to get bailed out. The GSEs were involved, but were not the most significant players. Mostly they were forced to compete with private firms. CRA mortgages amounted to maybe 10% and failed at half the rate of other subprime mortgages. This does not excuse the dealing of the GSEs, but the financial sector is one where there are very few whistle blowers. They were all trying to profit.

Both Pace and John Williams have to read a book titled “Reckless Endangerment.” The head of Fannie Mae in the 1990’s, James Johnson, was instrumental in rendering the federal regulating agencies powerless. Johnson also worked closely with Angelo Muzzio, the corrupt head of Countrywide, one of the largest private toxic loan lenders (60 Minutes did an expose of Countrywide a couple of weeks ago).

Fannie Mae got rid of regulation, bribed members of Congress, and showed private subprime lenders how to manipulate the system. They most certainly were a major player and a major cause of the crisis. By 2007, Fannie Mae alone had over $400 billion subprime loans on its books. While the private subprime lenders eventually surpassed Fannie Mae, their actions would not have been possible had Fannie Mae not corrupted the entire system.

The diagram omits several essential elements of the subprime mortgage crisis. (It’s a euphemism to call it a crisis. It’s also somewhat misleading to call it a “subprime mortgage crisis” since over half of foreclosed mortgages have been prime. In fact, the very name “subprime mortgage crisis” is a formulation adopted by anti-capitalists to smear the entire financial industry as predatory lenders that wrecked the economy.)

First, the State’s intrusion in mortgage finance began much earlier than the chart suggests. FNMA and FHA were established in 1938 as part of Roosevelt’s New Deal. Though the modern Fannie Mae (nee FNMA) was a publicly traded corporate entity, it was a creation of the State rather than the free market. Its mandate was defined by the State and it has always depended upon the State. Possibly even more significant, as Pace points out above, the establishment of the Federal Reserve in 1913 appears to have radically changed home mortgage finance. There has not been a truly free market in home mortgage finance since then.

Prior to the 1920s, credit ratings per se were not used to evaluate the worthiness of a potential mortgagor. Instead, the mortgagee relied upon the property’s productive or rental value, a substantial down payment (typically at least 50%), and the reputation of the mortgagor. It wasn’t until the 1920’s that the so-called Philadelphia Plan facilitated a down payment as low as 20%. You read that right: “a down payment as LOW as 20%”.

The reduction in down payment requirements is perhaps the single most important factor in the more recent financial disaster of 2008. See http://www.independent.org/newsroom/article.asp?id=2555.

During the 1920s, there was an explosion in mortgage lending. This was, no doubt, related to two important developments of the earlier decade: the establishment of the Federal Reserve and the sudden reduction of federal credit demand following the end of WW I. Housing starts in the 1920s peaked at about a million units per year; prior to WW I, the peak in housing starts was half that. In constant, inflation-adjusted dollars, expenditures for new dwelling units during the decade 1920-1929 was double that of any of the three prior decades. (1890-1899: $17.7B. 1900-1909: $18.6B. 1910-1919: $17.5B. 1920-1929: $37.2B. http://www.nber.org/chapters/c1320.pdf. See p. 64.) Can there be any doubt that this enormous expansion in residential construction and credit was facilitated by the Federal Reserve? Though commercial banks only accounted for 10-15% of direct mortgage lending during the 1920s, money and credit are fungible, and the effects of their expansion eventually permeate the entire economy. Further, the 1920s witnessed an explosion of private real estate securities, which could be purchased and held as investments by commercial banks, or used as collateral to borrow from commercial banks.

Federal Reserve policy since the late 1990s was also an essential element in the financial disaster of 2008.

Following the Asian currency crisis and the meltdown of Long Term Capital Management, the Federal Reserve has maintained an interest rate policy that has kept short-term real interest rates at or below zero, except for a brief period in 2006/2007. Ordinary savers had to become speculators just to retain the value of their savings. More sophisticated investors with access to cheap short-term credit had huge incentives to leverage their positions. The cheap credit conditions created by the Federal Reserve caused the nature of securities markets to transition from prudent long-term investment markets to casino capitalism.

Another point: The CRA — particularly the Clinton-era enhancement in enforcement — played a role in the subprime mortgage crisis. However, the role of the CRA illustrated in the chart was not as significant as many conservative commentators think. Far more significant was a derivative effect of the CRA lending. After it becomes accepted practice to make loans that fail to meet reasonable standards of creditworthiness for some borrowers, it will eventually become accepted that the old standards of creditworthiness are generally obsolete. And that is exactly what happened.

There is no better article on this than Stan Liebowitz’s “Anatomy of a Train Wreck”, which is available for free at http://johnrlott.tripod.com/Liebowitz_Housing.pdf.

At about 25 pages of readable prose, it is a concise, well-documented, and expert summary.

The point of the ancient history is that the expansion of credit facilitated by the Fed back in the 1920s parallels the credit expansion since the late 90s … with similar consequences.

The chart also misses a huge development in residential mortgages that occurred in the 1980’s: the collapse of the S&L industry. From 1975 to 1990, the S&L share of residental mortgage financing went from about 50% to about 15%. Fannie, Freddie, and agency financing grew by about the same amount. See Figure 2 in https://sedonaweb.com/attach/schools/NCBEfaculty/attach/chapter-297.pdf for relative market shares from 1895 to present.

Though fraud and political corruption were rampant, the S&L industry primarily collapsed because assets were grotesquely mismatched with liabilities. The entire industry was insolvent with a asset portfolio of ageing 30-year 6% mortgages matched against short-term deposits in a 12% short-term interest rate environment.That’s a rough description, of course: it was even worse than that in the early 80s, making clear that the S&L was an unsustainable business model.

Once again, Federal Reserve policy, coupled with federal deficits, were at the root of the S&L meltdown. Fed Chairman Paul Volker had to jack up interest rates in the late 1970s and early 1980s to kill the double-digit inflation that the Fed’s earlier easy money policies had caused. Similar to the more recent situation with Fannie/Freddie, the S&L industry lobbied hard for deregulation and regulatory relief. They got it in the form of the Depository Institutions Deregulation and Monetary Control Act and the Garn/St Germain Act, as well as relaxed regulatory and accounting practices. Ostensibly this was all done to save the S&L industry. Instead, fraud and corruption proliferated in the industry, and it ultimately flamed out in a $300 billion disaster paid for by taxpayers.

Thanks for all of the additional history, Bob.

Suggestions for how to squeeze it into a one-page flowchart?

“Suggestions on how to squeeze it into a one-page flowchart?”

That’s a problem. The current financial catastrophe is a multidimensional perfect storm of coercive altruism and its unintended consequences with heaping portions of rent-seeking, fraud and venality. It’s nigh impossible to depict all that on a single page.

However, I can make two suggestions for your consideration.

First, change the title to “The Failure of GSEs in the Subprime Mortgage Crisis” or something like that. Fannie and Freddie weren’t the only causes of this crisis. HUD played a huge role as did the Federal Reserve. And, American liberals are not entirely wrong in their criticism of private actors in investment banking, commercial banking, and mortgage origination. For some reason, few critics place any responsibility on the a government education system that utterly failed to educate its charges in either the proper use of credit or the responsibility to honor contracts.

Second, the quality of a mortgage is not properly dichotomized between “good-credit people” and “poor-credit people”. Strategic default has become a popular topic among heretofore “good-credit people” with upside-down mortgages in non-recourse states. Maybe something along the lines of the following re-wordings would be clearer.

“Mortgage lenders establish minimum down payment and credit standards”

“People who can make down payment and meet standards get loans”

“People who cannot make down payment or meet standards cannot get loans”

‘Racial minorities disproportionately unable to make down payment or meet standards”

…

“Lenders make poor quality loans at higher interest rates & then sell those loans to Fannie & Freddie”

“Poor quality loans appear to be profitable”

“Lenders make more poor quality loans”

…

New Item: “Increased demand inflates housing bubble that eventually bursts”

…

“Large number of poor quality loans in default” with a feedback loop to the new item above.

…

“Game Over: Government bailout and conservatorship of Fannie and Freddie”

There’s no need to say that the government “takes over” Fannie and Freddie: they’ve been GSEs all along. IIRC, the President appointed five of its directors before it went into conservatorship. As WSJ’s Paul Gigot put it: “The abiding lesson here is what happens when you combine private profit with government power. You create political monsters that are protected both by journalists on the left and pseudo-capitalists on Wall Street, by liberal Democrats and country-club Republicans.”

http://www.slate.com/articles/news_and_politics/press_box/2008/09/fannie_mae_and_the_vast_bipartisan_conspiracy.single.html

Good suggestions, Bob. I appreciate them.

Nonsense.

Derivatives are neither good or bad, no different than any tool. Are blow torches bad; a nonsense question.

Over pricing of debt lent to low quality borrowers is the pure and sole treason for the financial crisis. Why did investors over pay funding this debt. All reasons are rooted in Federal Government bias toward home ownership.

The financial crisis that exploded in 2008 was a asset bubble knowingly engineered by the Federal Reserve, the U.S. Congress, Wall Street “banks”, and a host of other actors. Yes, you can call this assertion a conspiracy theory if you want but I am only reciting the facts. The Fed’s role was to use their Open Market Committee to drive interest rates down until they were so low that it created a mountain of money that was almost free. As a result, an unending river of ultra cheap money flowed into the economy. Thousands of families took advantage of these extraordinarily low interest rates to take 30-year fixed mortgages to buy new houses. Next Wall Street “banks” began borrowing this cheap money to buy up these mortgages by the thousands. They leveraged themselves sometime 40 to 1 on borrowed money. They took these thousands of mortgages and piled them into packages called mortgage bonds and sold these bonds (rated AAA) as investments to their customers. The AAA rating came from the fact that ALL the mortgages were originally obtained by by borrowers who had FICO scores of 600 or above thereby making the rate of repayment of the mortgage about 97%. So, far so good. But then every mortgage seeker who had a FICO of 600 or above already had secured their mortgages. Did the Wall Street banks say “Well that was a good ride but it’s over? Not they did not. They fanatically pushed the creation of so called subprime mortgages. BUT at adjustable rates that would rise when interest rates rise. As interest rose, their mortgage rates rose and they defaulted by the tens of thousands, the mortgage bonds that these mortgages were piled into collapsed. And by the way, the junk mortgage bonds with all the junk subprime mortgages in them were also rated AAA by the rating agencies. The rating agencies just lied. They Wall Street “banks” simply put half high FICO scores and half low FICO scores until the AVERAGE score was 600. This was a big deception as half of the mortgages were sure to default due to the low FICO scores of half of the borrowers. Then the grossly over leveraged banks around the world began to fail. But not to worry, in the United States the U.S. Congress simply authorized the theft of a trillion taxpayer dollars to bail out the banks and their executives. The executives used billions of these tax payer dollars to give themselves massive multi million dollar bonuses. Not a single bank executive or financial player was ever indicted. These facts and they speak to the corruption that operates inside the world financial system.